What is bulk payment processing, and how does it impact businesses in 2026?

Bulk payment processing is the mechanism that allows organizations to process immediate, mass payments to multiple recipients (employees, suppliers, or partners) from a centralized account in a single transaction.

Imagine there are six days left until payroll or payments to critical suppliers. In the traditional model, your treasury team faces a chaos of massive Excel files, banking portals with slow interfaces, and the latent risk of human error when manually entering data.

This scenario is not only inefficient; it is an obstacle to the competitiveness of companies operating at scale.

Today, making disbursements based on restricted cycles is outdated and inefficient.

In this guide, we explore how the introduction of payment solutions—both regional and international—and payment orchestration are redefining modern treasury, ensuring that every payout is immediate, secure, and traceable.

How does digital disbursement optimize corporate treasury operations?

Historically, the standard in markets such as Colombia has been the use of flat files (.txt or .csv) uploaded to banking portals for processing via ACH (Automated Clearing House).

Under this system, the bank processes batches at scheduled times. If a treasurer forgets to upload a file before the 3:00 PM cutoff, hundreds of beneficiaries will not receive their funds until the next business day.

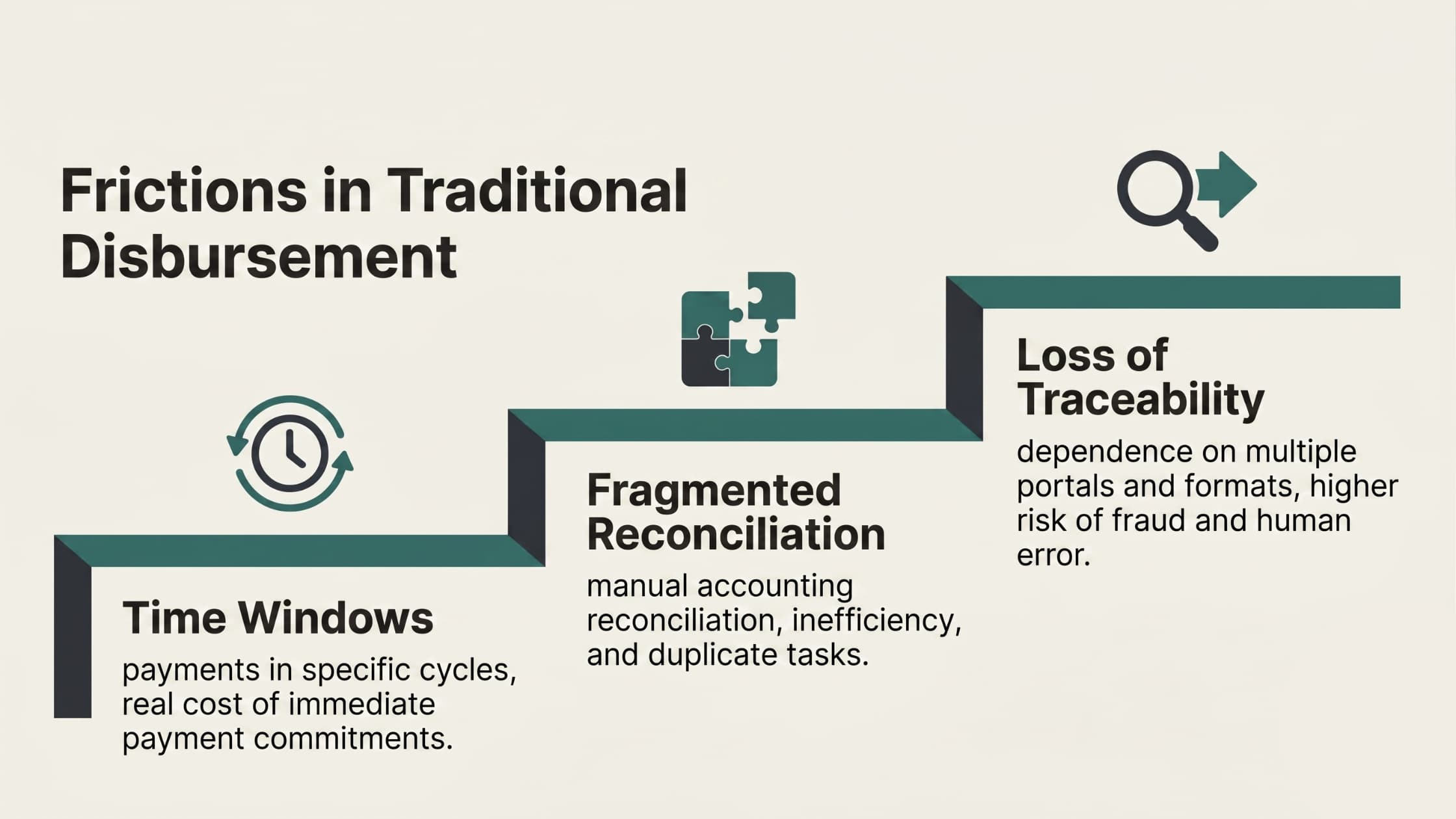

Friction in payroll processing through traditional treasury operations

The ACH model was designed in a context where immediacy was not a competitive factor.

However, the digital divide in Latin America is closing, and companies that still rely on manual processes face critical consequences that affect their cash flow and reputation:

Operating with time windows has a real cost when it comes to immediate payment commitments, as payments are processed in specific cycles; manual accounting reconciliation consumes resources such as time and human effort; finally, the reliance on operating across multiple portals and formats leads to more human errors and creates greater opportunities for fraud.

In contrast, modern payment distribution, driven by orchestration platforms like Cobre, breaks down these barriers by allowing the company to act as its own financial distribution hub, gaining autonomy over its timing and liquidity.

How does bulk payment distribution work technically?

For a CTO or a financial leader, understanding the internal processing of payment distribution is vital. The process follows a structured technical workflow that ensures funds reach their destination seamlessly, integrating directly with enterprise resource planning (ERP) systems.

How to enable payment distribution via API with Cobre?

While each case has details specific to the company’s needs, these are the three most important steps your company must follow to integrate the Cobre API into your payment distribution process.

Authentication and initial credential setup

Before sending any payment distribution request, you must complete two steps if you are already a Cobre customer:

- Obtain valid API credentials from the Cobre platform (Client ID / Secret) and exchange them for an access token.

- Use the token in the Authorization header for all subsequent API calls. This step is crucial for the API to identify and authorize requests from your system.

Set up and manage the necessary accounts and counterparties

Before initiating any payments, you must structure the cash flow in Cobre:

- Create or link Cobre Virtual Balance accounts. These accounts represent the funds available for disbursement.

- Register or manage counterparties. Counterparties are external entities such as beneficiaries, bank accounts, or customers to whom payments will be sent. This step ensures that the system recognizes the senders and recipients; that is, who sends and who receives money through Cobre

Create and execute money movements for the distribution of payments

Once authentication is complete and the lists of counterparties are prepared, the final step is to enable the endpoint: Create a Money Movement. This endpoint allows you to initiate a payment or disbursement order from an associated account to a counterparty.

There are four important parameters for this:

- The source account, source.

- The destination counterparty, destination.

- Amount to be paid, amount.

- Additional information useful for reconciliation, metada.

Optionally, you can add your own identifier for internal correlation: external_id.

Two other optional but important steps for the distribution are:

- Add a transaction approval step; this is especially relevant for workflows that require a review process.

- Create and schedule bulk transactions to automate disbursement at scale.

In summary, the three main steps to integrate the Cobre API into your disbursement processes are: first, authentication and credential configuration; second, account and counterparty configuration; third, initiating the money transfer: payment disbursement.

What is the operational scope of payment orchestration?

Not all banks speak the same technical “language.” This is where a global payments solution acts as a translator.

Orchestration allows a large company to send payments to 15 different banks from a single interface, consolidating cash visibility and reducing the technical complexity of maintaining multiple direct bank connections.

When and in what situations is bulk payment processing most useful?

Payment processing has evolved beyond traditional payroll. By 2026, its versatility makes it a strategic tool for making immediate payments across various industries.

Payroll and Salary Disbursements

This is the most widespread use. Automating payroll is critical for companies with more than 100 employees.

Immediate disbursement ensures that employees receive their pay even on non-business days, which dramatically improves the work environment and reduces the workload on the payroll team.

Payments to Suppliers (B2B Accounts)

In Latin America, manual payments involving multiple validations cause unnecessary delays. Bulk disbursement automates payments to recurring suppliers, facilitating accounting reconciliation and improving the company’s negotiating position by ensuring absolute punctuality.

Cashback and Automated Refunds

For the e-commerce and retail sectors, cashback is a powerful loyalty tool. Cashback programs in the region are expected to grow by 14% annually through 2029.

Processing these refunds individually would be a logistical nightmare; mass disbursement allows for the execution of thousands of incentive micropayments in seconds.

The Gig Economy and Freelancers

A mass disbursement payment solution is essential for last-mile platforms or professional services that need to pay thousands of independent workers for specific tasks. These payments are variable and high-frequency.

In fact, immediate payment is the key factor in retaining talent in the gig economy.

Incentive Payments and Commissions

Ideal for distributed sales forces. The ability to distribute performance bonuses instantly upon meeting a goal acts as a direct positive reinforcement for team productivity.

What are the strategic benefits of bulk and scheduled payouts?

For a CFO, automating payment disbursements has a direct impact on the income statement and risk management.

Cost Reduction and Resource Optimization

Automation reduces processing time by up to 90%. What used to take a treasury team a full workday is now completed in minutes.

This allows staff to focus on strategic financial analysis rather than mechanical data entry tasks.

Elimination of Human Error and Fraud

Typing errors are one of the leading causes of financial loss in manual transfers.

Electronic disbursement systems include automatic counterparty and check digit validations, as well as business rules that prevent duplicate payments or payments to unauthorized accounts.

Traceability and Regulatory Compliance

Each transaction is recorded with a timestamp, a unique ID, and a verified recipient. This simplifies audits and ensures that the company complies with local transparency and anti-money laundering regulations (SARLAFT/AML).

For example, automated payroll disbursement connected to SPEI for business use has the advantage that these transfers generate a CEP, a tamper-proof document with fiscal validity.

Recipient Satisfaction and Brand Reputation

Timeliness is the foundation of trust. Whether it’s an employee waiting for their paycheck or a supplier awaiting payment of an invoice, the immediacy of electronic disbursement strengthens business relationships and improves the organization’s credit rating.

The Real-Time Payments Revolution in Latin America

The barrier of banking cycles is falling. By 2026, waiting 24 hours for funds to clear will no longer be considered an acceptable standard, but rather a technical shortcoming.

SPEI, Pix, and more recently Bre-B in Colombia are setting a new standard for what efficient treasury management looks like.

What is Bre-B and why is it a game-changer in Colombia?

Bre-B is the new instant payment system managed by the Central Bank of Colombia. Its implementation enables full interoperability: transferring money between banks and digital wallets using only an identifier (such as a cell phone number) with funds credited in less than 20 seconds.

For payment processing, this means that companies are no longer "held hostage" by clearinghouse schedules.

Liquidity becomes truly liquid, enabling 24/7 operations. Cobre, as the orchestrator, integrates this immediacy so that corporations can use Bre-B on a massive scale without needing to redesign their entire internal infrastructure.

Crypto Mass Payments: Stablecoins in Corporate Treasury

Although the use of digital assets is still in the early stages of regulatory adoption, mass payouts using stablecoins—fiat-backed cryptocurrencies—offer an unprecedented solution for companies with cross-border operations.

Stablecoins enable international payments while eliminating correspondent banking costs and last-minute exchange rate fluctuations.

You can read more about what a stablecoin is and its uses for B2B collections and payments.

What to Look for in a Global Payments Solution?

Not all disbursement platforms are created equal. A CTO must evaluate specific technical criteria to ensure scalability:

- Interoperability: The platform must allow frictionless payments to any financial institution, cooperative, or digital wallet.

- Scalability: It must support the processing of thousands of simultaneous transactions without service degradation (especially during peak periods such as paydays or year-end).

- Multi-Layer Security: Multi-factor authentication (MFA), end-to-end encryption, and security certifications such as PCI DSS are essential.

- Agile Integration: Clear API documentation and robust technical support reduce time-to-market.

- Data Intelligence: Analytics tools that enable the visualization of spending patterns and the optimization of cash flow in real time.

How to Avoid the Most Common Errors in Payroll Disbursements?

Despite technological advancements, operational oversights can still compromise a disbursement. Here’s how to mitigate them:

- Failure to Validate CLABEs/Accounts: The most common error. The recommendation is to add a layer of automatic pre-validation to the disbursement platform.

- Failure to update payroll databases: Maintaining records for employees who no longer work there or outdated salary figures. The best practice is to implement a direct integration between HR software and the payment system.

- Reliance on a single institution for payouts: Relying on a single bank to process payments can be problematic in extreme cases of a system outage. Using an orchestrator that allows switching between multiple funding sources is a practice that prevents these cases, which, although rare, do occur.

From Cost Center to Competitive Advantage

By 2026, payment distribution has evolved from an administrative task into a tool for business agility.

Companies that adopt instant bulk payments and orchestration not only save time; they gain the ability to react faster than their competitors, retain their talent, and optimize every penny of their liquidity.

Financial digital transformation starts at the foundation: how we move money to those who make the business possible. Electronic disbursement is the first step toward an autonomous, intelligent, and global treasury.

FAQ’s about Electronic Disbursement

How long does a payment disbursement take?

It depends on the system. Under the traditional ACH model, it can take 4 to 24 business hours. With instant payment systems such as Bre-B or SPEI, settlement is instantaneous (seconds) and operates 24/7.

Is it safe to distribute payments via API?

It is significantly safer than manual file handling. APIs use encryption protocols and security tokens that eliminate the risk of data tampering during transit.

What is the difference between a bulk transfer and a disbursement?

Although they are used interchangeably, a disbursement involves a process of managing funds from a central account to multiple beneficiaries based on business logic (validation, scheduling, and automatic reconciliation), whereas a bulk transfer may simply involve sending a batch without any further operational intelligence.