Payment Orchestration: The Complete Guide for Modern Businesses

This comprehensive technical guide covers all you need to know about payment orchestration solutions for your large-scale enterprise. How to address the specific operational needs of businesses growing into Latin America, and the core criteria for selecting an institutional-grade platform.

Key takeaways:

- Expanding B2B operations in LATAM is an opportunity

- The three layers on a payment orchestration platform

- How to leverage orchestration for faster settlement and bank reconciliation

For US enterprise leaders, expanding corporate operations into Latin America presents a massive growth opportunity. Driven by structural digitalization and a fast-evolving corporate environment, the region has become a primary destination for global commerce.

However, treasury departments trying to manage cross-border B2B transactions often face a stark realization: managing high-ticket money movement across Latin American markets requires navigating a complex and highly fragmented financial landscape.

When managing large-volume business operations relying on traditional banking networks leads to significant operational friction.

High FX markups, multi-day delays, manual accounting processes, and fragmented local payment structures regularly slow down enterprise treasury workflows. To solve these challenges, a new financial architecture has emerged: payment orchestrators.

1. What is a Payment Orchestrator?

A payment orchestrator is a unified software layer that centralizes, automates, and optimizes the end-to-end lifecycle of financial transactions by connecting multiple payment rails, banks, and clearing houses through a single integration.

Instead of building and maintaining custom, separate connections to every single domestic banking network, international wire service, and local clearing house, an enterprise uses a payment orchestration platform to act as an intelligent gateway.

The platform dynamically routes financial transactions across different networks, ensuring fast processing times, low transaction fees, and high success rates.

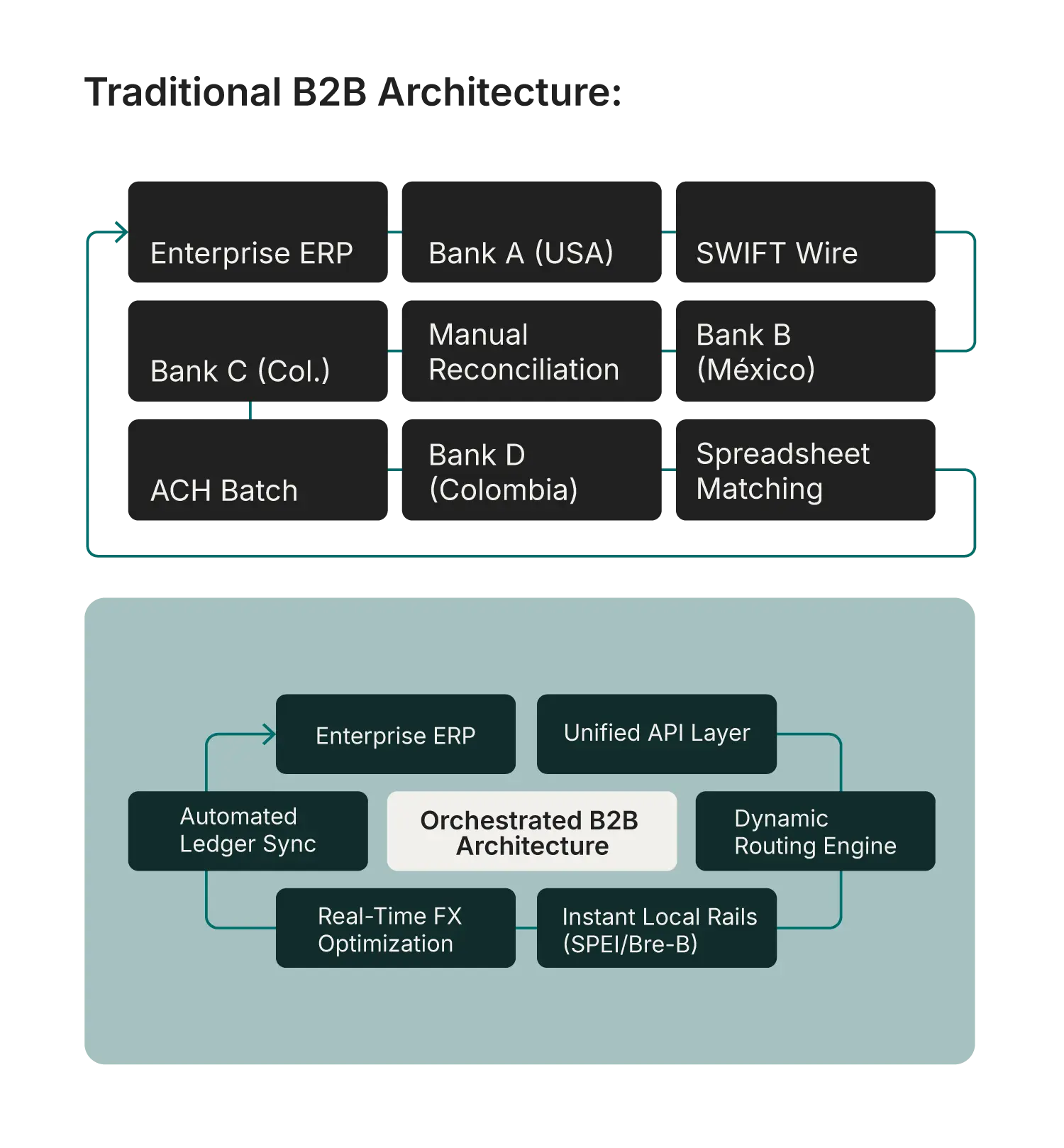

The Three Operational Layers of Payment Orchestration Platforms

To support enterprise-grade B2B transactions, top payment orchestration hub vendors deploy their infrastructure across three distinct functional layers:

- The Connectivity Layer: A single API integration that abstracts the underlying infrastructure. It communicates simultaneously with various legacy enterprise resource planning (ERP) platforms, core corporate bank databases, domestic automated clearing houses (ACH), and digital multi-currency accounts.

- The Routing Engine: An automated software layer that evaluates every payout request in real time based on currency, destination, transaction size, and local clearing schedules. It automatically determines the fastest, most cost-effective path to execute the transaction.

- The Settlement and Reconciliation Layer: A centralized data framework that consolidates multi-bank transaction data into uniform reporting streams. It delivers immediate updates via secure webhooks, cutting down on manual treasury tasks and keeping accounting ledgers accurate.

2. The reality of Latin American financial infrastructure

Expanding high-ticket corporate operations into Latin America means dealing with deep structural fragmentation. Every country operates under its own distinct regulatory framework, distinct central bank mandates, and unique local payment networks.

For US treasury teams, managing these distinct networks individually often requires months of specialized development, significant capital commitments, and continuous operational overhead.

Colombia: Real-Time Rails and the Bre-B Network

Colombia’s corporate payment landscape is undergoing a major transformation driven by the Central Bank's modern real-time clearing initiatives.

- The Bre-B Network: Modeled after successful instant-payment systems globally, the Bre-B network enables instant, interbank B2B fund transfers operating 24/7/365. Businesses can trigger real-time payments using static or dynamic keys, eliminating the multi-hour or next-day clearing delays common with traditional Colombian ACH systems.

- Cobre Fast Pay & Local Rail Access: Enterprise platforms like Cobre provide direct integration into these local payment rails. This setup lets global enterprises execute instant disbursements and high-volume payins via direct debit systems and real-time processing hubs without facing restrictive volume ceilings.

Mexico: High-Volume SPEI Integration

In Mexico, successful B2B money movement depends entirely on direct, scalable access to the central bank's electronic funds transfer system.

- The SPEI Network: Mexico’s Sistema de Pagos Electrónicos Interbancarios (SPEI) is one of the world's most robust real-time gross settlement systems, processing high-ticket business payments instantly using 18-digit CLABE account numbers or dedicated SPEI cards.

- Virtual CLABEs for Collection: For large enterprises handling collections from thousands of commercial buyers or distributors, tracking incoming payments can be difficult. A payment orchestration such as Cobre’s solves this by dynamically issuing unique virtual CLABEs. When a corporate client sends a payment via SPEI, the unique identifier maps directly back to that specific transaction, enabling fully automated, real-time matching and reconciliation.

3. What are the core enterprise needs for B2B operations in LATAM?

Large organizations managing multi-market supply chains, international logistics, or regional contractor networks face distinct treasury pressures that standard merchant-facing payment gateways simply aren't designed to handle.

Streamlining Bulk Corporate Payouts

Managing high-ticket supplier invoices or regional payroll using manual spreadsheet uploads across different banking portals is an inefficient use of resources and introduces high operational risk.

True optimization comes from deep architectural centralization, straight-through processing (STP), and end-to-end automation via API.

By establishing a single connection point to a payment orchestration hub, an enterprise treasury desk can instantly initiate thousands of concurrent payouts.

The platform checks account details, routes the money across domestic rails, and tracks every transfer in real time, transforming a multi-day process into a hands-off, few-minute workflow.

Minimizing International B2B Transaction Expenses

For companies moving funds globally, the primary drain on capital isn't standard outbound wire fees; it stems from hidden inefficiencies within the transaction lifecycle:

4. Key Factors to Consider When Selecting a B2B Payment Orchestrator

Choosing an institutional-grade platform requires evaluating specific technical and operational capabilities to ensure it can support long-term regional growth.

Multi-Rail Capabilities and Local Network Integration

A payment orchestrator must offer deep, native integration into local clearing infrastructure, rather than simply wrapping old international wire networks in a new API.

The platform should seamlessly bridge international workflows with core local payment rails. This ensures your treasury team can transition fluidly between cross-border funding and local real-time distribution.

Advanced Cross-Border Optimization and FX Controls

Market volatility across emerging Latin American economies can quickly erode corporate profit margins if foreign exchange execution is left unmanaged.

Look for platforms providing advanced capital protection tools:

- Rate Lock Protections: This capability of Cobre allows corporate treasurers to freeze an exact currency exchange rate for a designated time before funding a transaction. Securing the rate upfront insulates international B2B transfers from intraday market swings and ensures predictable payment amounts for suppliers.

- Short-Term Overdraft Credit Facilities: To keep critical supply chains moving, enterprise platforms can offer short-term overdraft liquidity options. This allows businesses to trigger urgent, high-ticket supplier distributions immediately without needing to pre-fund local custody accounts, optimizing working capital efficiency.

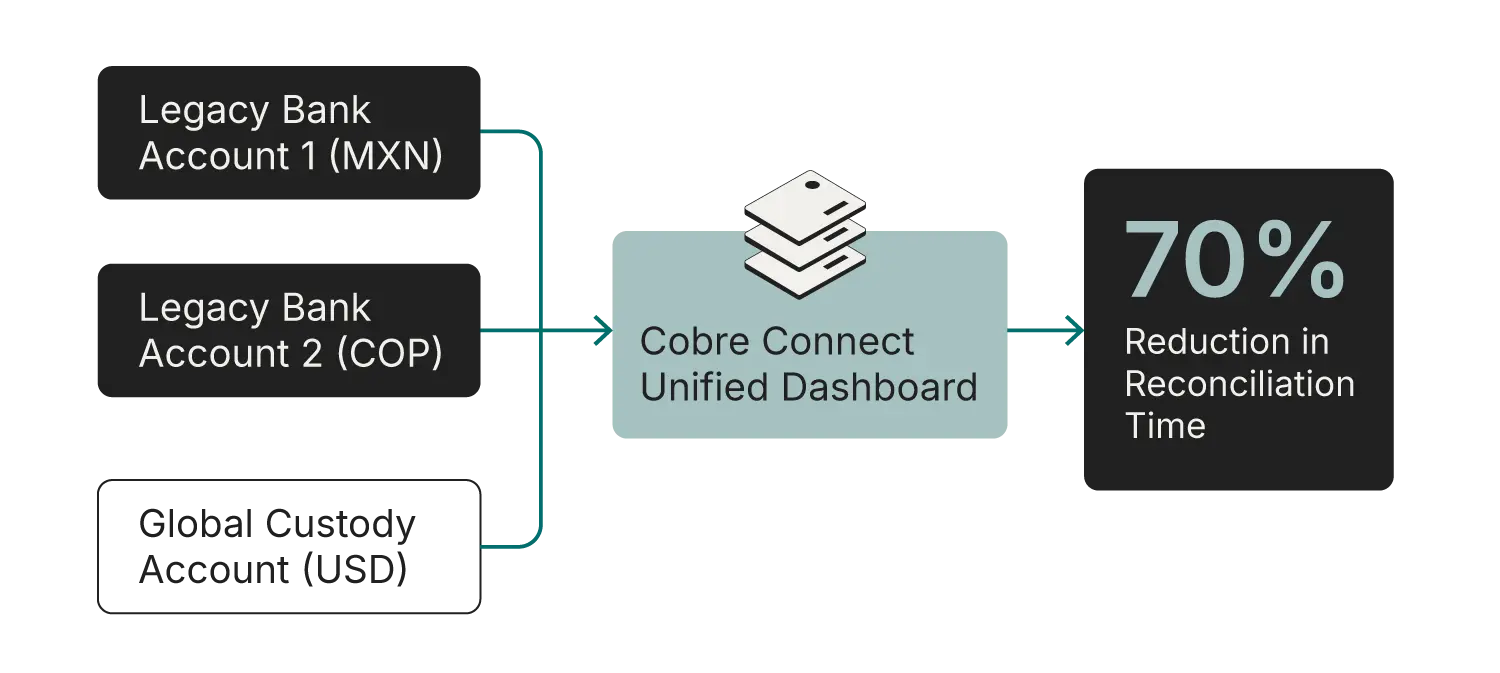

Multi-Currency Treasury Centralization

Large enterprises often operate across multiple local bank accounts, leading to fragmented visibility, disjointed cash management, and complicated treasury reporting.

Solutions like Cobre Connect fix this by consolidating diverse corporate bank profiles into a unified dashboard.

By unifying multi-bank architectures under a single interface, financial controllers can initiate instant ACH and real-time transfers directly from existing corporate balances without needing to pre-fund intermediate third-party wallets.

This centralized visibility eliminates manual bank portal hopping and reduces manual accounting reconciliation times by up to 70%.

Enterprise Stablecoin Architecture

For forward-thinking treasury teams, modern payment orchestration solutions leverage fiat-backed stablecoin infrastructure to complement traditional banking rails, helping bypass legacy processing bottlenecks and market downtime.

Global Settlement via Digital Dollars: High-tier orchestrators enable organizations to distribute USD-pegged tokens (such as USDC, USDT, and RLUSD) across leading, secure corporate blockchain networks including Ethereum, Solana, Polygon, Base, and Tron.

These transfers route directly to fully verified corporate entities and legal counterparts, enabling sub-minute settlement windows around the clock.

Institutional-grade compliance, verification, and security

Handling high-ticket corporate payments requires rigorous fraud prevention and strict adherence to global regulatory standards. A premier B2B orchestrator must feature institutional-grade security guardrails:

- Automated counterparty account verification: To prevent costly payment rejections and intercept phishing attempts, the platform should programmatically cross-reference recipient identifiers against official central banking registers before executing any funds transfer. This steps ensures the destination account name matches the business records, drastically reducing error rates.

- World-Class Security Certifications: The underlying technology must be audited and certified under top-tier global security standards, including ISO/IEC 27001:2022, SOC 2 Type II, and PCI DSS v4.0.1.

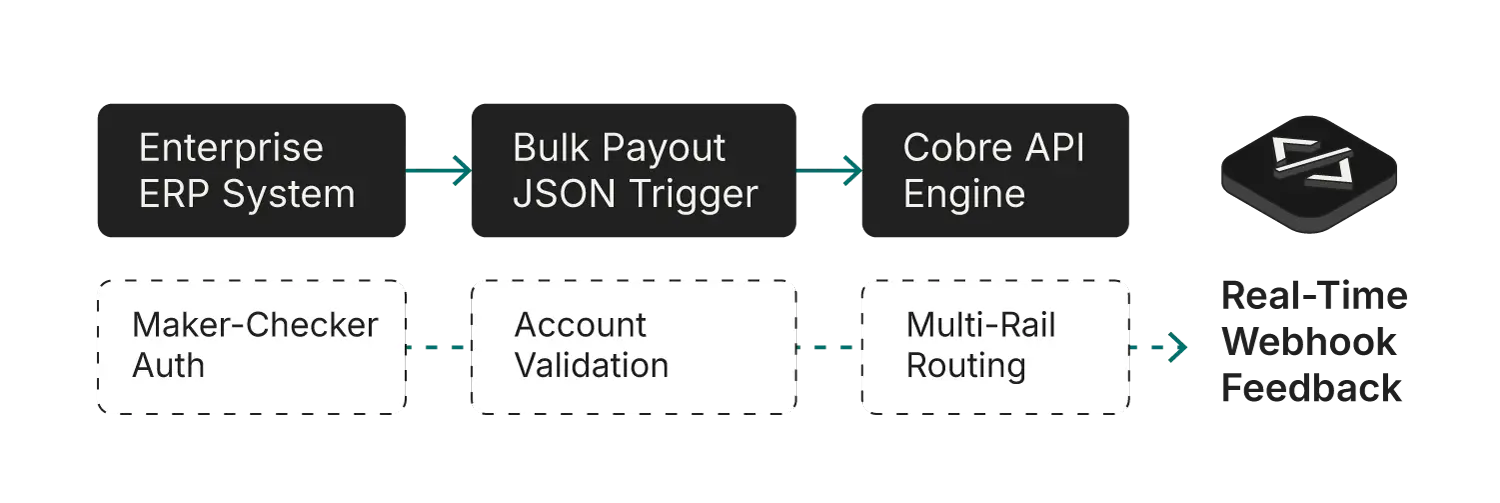

Developer-First API Integration and ERP Automation

A payment platform is only as valuable as its ease of integration into your existing business workflows.

High-throughput enterprise operations require an API-first approach that easily embeds into systems like SAP, Oracle, or Microsoft Dynamics.

This technical framework allows organizations to run bulk money movements simultaneously, enforce rigorous multi-tiered Maker-Checker approval workflows within their engineering systems, and leverage low-latency Webhooks to instantly feed transaction logs back into corporate accounting ledgers.

5. Enterprise implementation strategy: The migration path

Moving from a fragmented multi-bank setup to an automated, orchestrated system doesn't require overhauling your entire existing infrastructure overnight.

A phased implementation approach ensures a smooth, risk-mitigated transition:

- Phase 1: Centralization & Visibility: Connect your existing regional bank accounts to a central orchestration dashboard. This grants your global treasury team immediate, unified visibility into cash positions and settlement histories across markets without altering your current payment routing.

- Phase 2: Automated Workflows & Bulk Payouts: Integrate the orchestrator’s API endpoints directly into your ERP or accounting software. Begin routing batch distributions, supplier invoices, and local payroll through the automated engine to reduce manual intervention and standardize data streams.

- Phase 3: Full Optimization: Turn on advanced features like real-time local clearing, currency Rate Locks, and alternative global settlement mechanisms like corporate stablecoins to maximize cost savings and efficiency.

Future-Proofing Corporate Treasury

Expanding across borders shouldn't stall due to fragmented regional banking rails or slow manual reconciliation processes. For enterprise leaders driving expansion into Latin America, payment orchestration is no longer a luxury—it is a core operational requirement.

By abstracting financial fragmentation through a single API layer, platforms like Cobre allow global businesses to operate directly within local networks across Colombia and Mexico.

Centralizing multi-bank visibility, automating bulk B2B distributions, protecting capital with proactive FX rate locks, and leveraging stablecoin settlement mechanisms enables your treasury to run as an agile, scalable engine.

Your business is unstoppable. Partnering with the right payment orchestration platform ensures your money is too.

Frequently asked questions about payment orchestrators for LATAM operations

What is the difference between a payment gateway and a payment orchestrator?

A payment gateway connects your business to a single payment processor. A payment orchestrator sits above multiple gateways and rails to route transactions based on cost, success rate, or geography.

Do payment orchestrators replace existing PSPs in LATAM?

No. Orchestrators typically sit on top of existing PSPs and payment providers, adding a routing and management layer rather than replacing underlying processors.

How long does it take to integrate a LATAM payment orchestrator?

Integration timelines vary by provider and complexity. API-first orchestrators can typically be integrated in days to weeks rather than the months required for direct bank integrations.

Can a payment orchestrator operate in LATAM without a local entity?

Some orchestrators operate through local licensed partners, while others hold direct licenses. Verify whether the provider's structure meets your compliance requirements in each target country.

How do payment orchestrators handle PIX, SPEI, and PSE differently?

Each rail has unique technical specifications, settlement windows, and regulatory requirements. A capable orchestrator abstracts these differences behind a unified API while applying country-specific logic for formatting and compliance.