What is KYC (Know Your Costumer)?

KYC stands for Know Your Customer. It is a fundamental process used by companies to verify the identity of their clients and assess the risks associated with a business relationship. For financial teams, having a clear understanding of this concept is the first step toward secure and compliant cross-border operations.

In the complex world of compliance management and global finance, the term KYC is frequently used, for it’s a crucial tactic within Anti Money Laundering (AML) programs.

In this article we explain what are the key elements of KYC, and why is it so critical for businesses looking to expand their operations into Latin American markets like Mexico and Colombia?

What does KYC mean in business?

For organizations operating internationally, understanding the impact of this mechanism on the financial ecosystem is indispensable for three specific reasons:

- Strong correspondent banking relationships: Global financial institutions facilitate the movement of capital efficiently when businesses maintain transparent verification standards.

- Strict regulatory compliance: Corporations must adhere to local and international regulations regarding the prevention of money laundering and terrorist financing.

- Mitigation of fraud and operational risks: Verifying data from accounts and beneficiaries constitutes the primary defense against identity theft and opaque transactions.

What are the KYC requirements?

To operate securely across borders, businesses must gather precise information from the entities they do business with and adhere to strict know your customer requirements. The key elements of the corporate validation process include:

The core pillars of AML compliance: from onboarding to continuous monitoring

Modern financial compliance is not a single static check. It is a continuous lifecycle divided into clear operational protocols based on identity, risk level, and real-time behavior.

Ultimately, KYC is just one component of a broader, more complex process used to assess the risks of doing business with other companies.

The onboarding phase: verifying identities (CIP, KYC, & KYB)

Before any business relationship begins, institutions must verify the fundamental identity of the counterparty. This phase relies on three primary protocols:

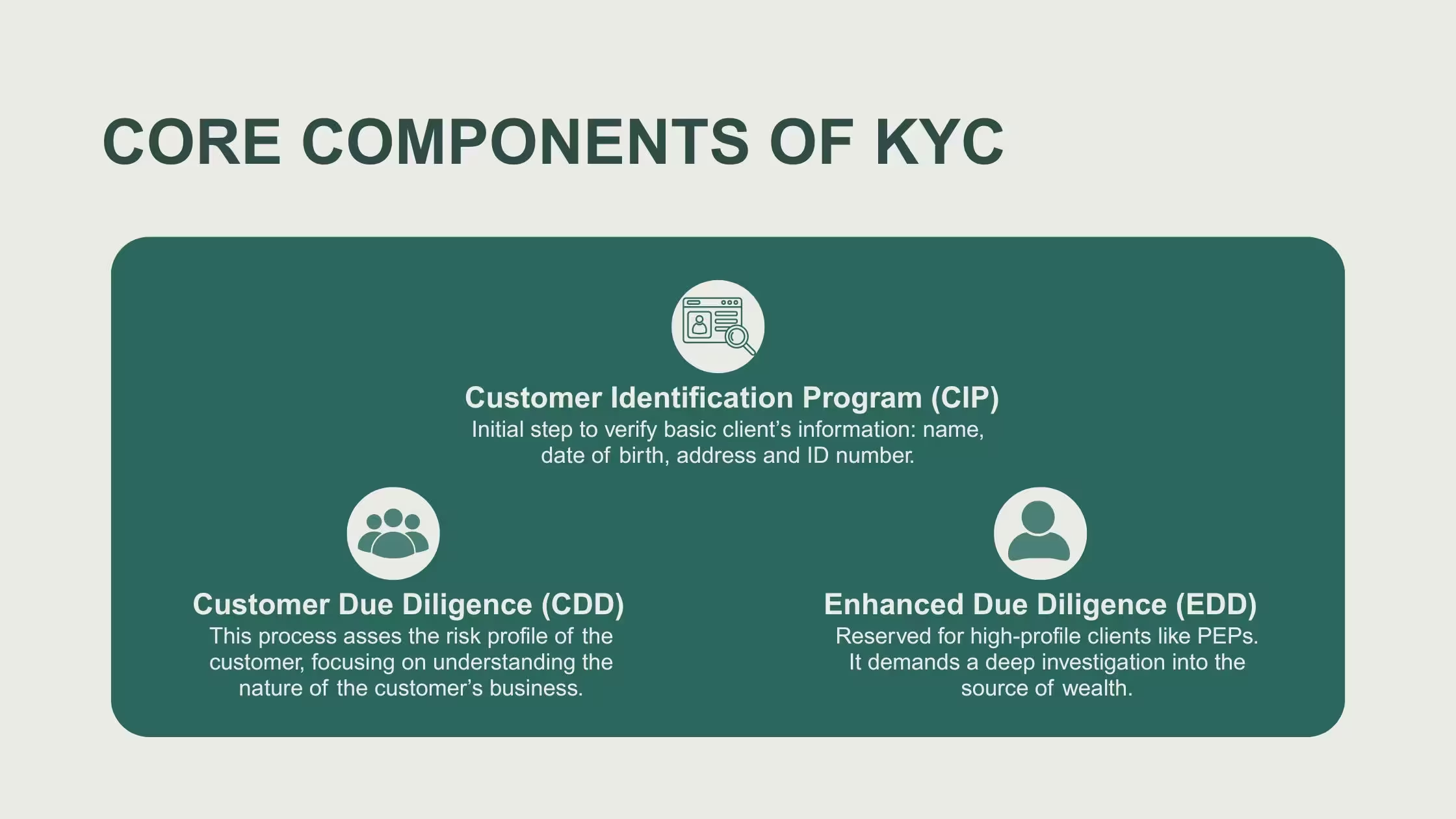

- Customer Identification Program (CIP): The baseline, mandatory onboarding stage required by regulatory frameworks. CIP focuses on the raw collection and initial verification of core data—such as legal names, tax identification numbers, and addresses—to form a verified identity profile before accounts are opened.

- Know Your Customer (KYC): The broader protocol that utilizes the CIP data to assess the potential risks associated with an individual, ensuring they are exactly who they claim to be.

- Know Your Business (KYB): A specialized adaptation of the KYC process focused exclusively on corporate entities. It analyzes corporate registries, operational licenses, and ownership structures to verify complex legal entities rather than single individuals.

Technological Execution Methods during Onboarding:

Depending on infrastructure, these identities are verified through three methodologies:

- Digital Verification (e-KYC): Conducted entirely online via API connections that cross-reference user data against government databases in real time, complemented by biometric controls.

- Video KYC: A remote, live interaction where a company’s legal representative streams with a compliance officer to validate original physical documentation.

- Traditional Physical Verification: A manual, paper-heavy process requiring the presentation of physical documents at a branch, which inherently increases processing times.

The Risk Assessment Phase: Customer Due Diligence (CDD)

Once an identity is verified, institutions apply varying levels of scrutiny based on the customer’s risk profile:

- Simplified Due Diligence (SDD): Applied to low-risk accounts or counterparties where identification thresholds are minimal.

- Standard Customer Due Diligence (CDD): The baseline operational protocol for most corporate accounts, focused on cross-checking company information against global screening lists and identifying Ultimate Beneficial Owners (UBOs).

- Enhanced Due Diligence (EDD): Reserved for high-risk accounts, such as entities from sanctioned countries or Politically Exposed Persons (PEPs). This requires a deep, exhaustive audit of the partners' source of wealth.

The Continuous Lifecycle: Ongoing Monitoring (KYT & pKYC)

Compliance shifts from static verification to real-time behavioral tracking once an account is active.

Know Your Transaction (KYT)

While KYC protocols assess risk before a transaction occurs, Know Your Transaction (KYT) continuously monitors the actual movement of money post-onboarding. It detects red flags and criminal patterns based on financial data through three steps:

- Data Analysis: Automatically screens transaction metadata (amounts, origins, and patterns) against historical behavior and global watchlists.

- Risk Assessment: Evaluates the transaction's risk score based on geographic threats, transfer velocity, and user profiles, flagging suspicious anomalies.

- Reporting: Triggers instant alerts for compliance teams and automatically generates Suspicious Activity Reports (SARs) to meet regulatory mandates.

Structural Optimization Ecosystems:

To keep this continuous lifecycle efficient, institutions leverage modern database approaches:

- Perpetual KYC (pKYC): Automation of risk profile analysis continuously over time, detecting unusual variations in operational behavior rather than relying on a single static annual review.

- Centralized KYC (CKYC): Secure, shared registries where a corporation's identity is validated once, avoiding repetitive paperwork across multiple ecosystem partners and financial allies.

Legal regulations and framework

In practice, KYC verification is the operational step of cross-checking provided identification data against official government records and local legal frameworks. For an american business operating internationally, KYC verification means ensuring that its counterparties' information matches the official registries of those target countries.

Adhering to local Anti-Money Laundering (AML) legal frameworks is mandatory to prevent operational bottlenecks, penalties, and rejected payments.

Far from restricting operations, proactive compliance frameworks are designed to channel cross-border digital transactions securely.

Nevertheless, understanding KYC regulations means navigating an interconnected web of international standards, national laws, and industry-specific requirements, designed to protect the global financial system from abuse.

International standards for AML

The Financial Action Task Force (FATF) sets global standards for combating money laundering and terrorism financing. These recommendations form the foundation for KYC regulations in over 200 jurisdictions worldwide.

Think of FATF as the architect drawing the blueprints. Individual countries then build their own structures based on those plans.

United States requirements and frameworks regarding AML

US businesses face multiple overlapping frameworks when it comes to money laundering prevention:

- Financial Crimes Enforcement Network (FinCEN) provides clear guidance on compliance obligations, helping businesses understand exactly what's required to stay protected and compliant.

- The Bank Secrecy Act (BSA) established the foundation in 1970, requiring financial institutions to help government agencies detect and prevent money laundering. It protects both financial institutions and their clients by establishing clear verification standards.

- The USA PATRIOT Act expanded these requirements after 2001 adding enhanced due diligence for foreign accounts and correspondent banking relationships. Section 326 mandates Customer Identification Programs (CIP) that protect businesses from unknowingly facilitating illicit activity.

- Office of Foreign Assets Control (OFAC) maintains sanctions lists that protect US businesses from inadvertent violations. Regular screening against these lists shields your company from legal and reputational risk.

Canadian framework for AML

Canadian requirements center on the Proceeds of Crime (Money Laundering) and Terrorist Financing Act, enforced by the Financial Transactions and Reports Analysis Centre (FINTRAC).

The framework mirrors US protections in scope while providing clear Canadian-specific guidance. US companies expanding to Canada benefit from mature, well-documented compliance standards.

Frameworks for AML in Latin American Context

For US and Canadian companies doing business in Latin America, regional frameworks provide additional security layers:

- Colombia's Sistema de Administración del Riesgo de LA/FT (SARLAFT) sets rigorous standards that protect both financial institutions and their clients. The Superintendencia Financiera provides clear enforcement guidelines that help businesses understand exactly what's expected.

- Mexico's Unidad de Inteligencia Financiera (UIF) emphasizes transaction monitoring alongside identity verification, creating comprehensive protection against financial crime. Recent regulations requiring beneficial ownership disclosure add transparency that protects legitimate businesses.

- Brazil's Consejo de Control de Actividades Financieras (COAF) coordinates AML efforts with sector-specific requirements that adapt to different business models. Recent expansions to fintechs and payment platforms ensure consistent protection across the ecosystem.

What are some of the industry-specific layers to AML/KYC?

- Payment Service Providers (PSPs): Face stringent licensing requirements that mandate comprehensive, continuous KYC standards.

- Money Transmitters: Must register with FinCEN and actively comply with diverse state-level regulations.

- Fintech Platforms: Must navigate varying frameworks depending on their services. For example, a platform offering both payment processing and FX services simultaneously faces requirements from banking regulators, payment oversight bodies, and commodities authorities.

- Stablecoins & Crypto Rails: The rise of digital asset payments introduces an entirely new layer of international oversight. Cross-border liquidity moving via blockchain rails must now comply with strict, emerging regional frameworks, such as the MiCA Regulation in the European Union and the GENIUS Act in the United States, which enforce strict reserve transparency and strict user verification. You can read more about stablecoin regulations.

The Modern Infrastructure Solution

Modern payment infrastructure built for North America-to-Latin America corridors handles this multi-layered complexity automatically.

Navigating these fragmented traditional and crypto frameworks independently is highly complex and error-prone. A robust, unified payment infrastructure solves this by managing multi-jurisdiction compliance natively.

Instead of burning valuable time and resources trying to become regulatory experts in every region, partnering with specialized platforms like Cobre ensures your operations are fully compliant from day one.

How does a financial infrastructure benefit your KYC process?

Strong KYC processes separate companies that scale confidently from those constantly managing crises, costing them not only money, but reputation as well.

Build correspondent and strong banking relationships

US banks scrutinize the compliance programs of every business client, especially those processing cross-border payments.

Companies with robust KYC practices maintain stable banking relationships, faster wire processing, and access to better payment infrastructure.

When your bank sees comprehensive verification processes, payments flow smoothly. Your account stays active. The relationship strengthens over time.

Companies processing high volumes of cross-border payments to Latin America need infrastructure that handles KYC verification.

Payment acceptance rates climb with proper KYC

Financial institutions process payments from properly verified sources faster and with fewer holds. If you're paying suppliers in Latin America, thorough KYC means:

- Payments clear on first attempt

- No delays waiting for additional verification

- Stronger supplier relationships built on reliability

- Working capital moving efficiently

Companies with robust KYC processes report fewer payment rejections on cross-border transactions.

Regulatory compliance protects your operations

Comprehensive KYC ensures:

- Uninterrupted access to banking services

- Maintained money transmitter licenses

- Protected executive reputation

- Competitive advantage through operational stability

More importantly, it demonstrates to regulators that you take financial crime prevention seriously, positioning your company as a trustworthy player in cross-border and local commerce.

Fraud prevention saves real money

KYC procedures catch identity theft, business email compromise, and vendor impersonation before they drain bank accounts. According to the Association of Certified Fraud Examiners, companies with strong verification processes lose 50% less to fraud than those with weak controls.

Every fraudulent payment prevented is capital preserved and relationships with suppliers and banks protected.

Protection from sanctions violations and money laundering

Perhaps the most critical benefit of a thorough KYC is protecting your company from unknowingly doing business with any of the following:

- Sanctioned entities or individuals

- Shell corporations used for money laundering

- Front companies for criminal organizations

- Businesses in restricted jurisdictions

The reputational damage from a single sanctions violation or money laundering connection can take years to repair, if recovery is possible at all.

The competitive advantage is clear: Companies that verify thoroughly while onboarding efficiently win more business and scale faster. They build supplier networks confidently, knowing every relationship has been properly vetted.

Grow your international transactions securely with Cobre

Expanding your business into Latin America requires an infrastructure partner that understands both the regulatory landscape and the need for operational speed. Cobre acts as a centralized financial infrastructure that allows US businesses to manage international transactions efficiently.

With Cross Border, you can fund your operations in USD and execute payouts in local currencies (such as MXN and COP) in real-time. Cobre allows you to safely orchestrate your payments, ensuring that your corporate payouts comply with local standards without sacrificing speed.

Discover how we can streamline your operations in Latin America and optimize the efficiency and security of your global transactions. Contact our team to integrate an API first payment infrastructure aligned with your organization's needs.

FAQs about KYC and regulatory compliance

What's the difference between KYC and AML?

KYC is part of AML, not separate from it. Think of AML as the entire house and KYC as the foundation. KYC focuses on verifying who your customers are and what risk they pose. AML is the broader framework that includes KYC plus transaction monitoring (KYT), suspicious activity reporting, and other controls to prevent money laundering.

What are the three components of KYC?

- Customer Identification Program (CIP) verifies digital identity through document verification and data validation.

- Customer Due Diligence (CDD) assesses risk based on profile, geography, and business type.

- Ongoing monitoring transaction patterns and updates information periodically.

What is SDD and EDD?

- SDD (Simplified Due Diligence) applies to low-risk customers. It requires minimal verification and basic documentation.

- EDD (Enhanced Due Diligence) applies to high-risk situations. It requires extensive verification including source of funds, business purpose documentation, and continuous monitoring.

For whom is it mandatory to have EDD verification?

EDD, Enhanced Due Diligence, is mandatory for politically exposed persons, high-risk jurisdictions, and complex corporate structures.

What is identity verification in KYC?

Identity verification confirms that a person or business is who they claim to be. For individuals it validates government IDs, matches biometrics, and cross-checks databases. For businesses, it confirms corporate existence, identifies beneficial owners, and validates authorized signatories.

Modern systems use OCR, facial recognition, liveness detection, and real-time database checks.

How long is KYC valid?

Low-risk profile typically need updates every 12-24 months. Medium customer risk every 6-12 months. High-risk customers require quarterly or monthly updates.

Changes in ownership, business operations, or significant transaction patterns trigger immediate re-verification regardless of timing.

What is KYC in banking?

Banks use KYC to verify customer identity, assess risk, and monitor relationships throughout their duration. They face the strictest requirements as primary gatekeepers preventing financial crime.

Your KYC quality directly affects your banking relationship quality and access to services.

Is KYC the same in every country?

No. While FATF provides a common framework, requirements vary significantly by jurisdiction.

Documentation differs (US needs SSN, Mexico needs RFC, Colombia needs NIT). Transaction thresholds, risk assessments, and timelines vary by country.

For cross-border operations, you must comply with all applicable jurisdictions simultaneously. A US company paying Mexican suppliers needs to satisfy both FinCEN and UIF requirements.