Payment rails: A guide to global money movement systems

Payment rails: A guide to global money movement systems

According to McKinsey's Global Payments 2025 report, as of September last year, the payments industry generated $2.5 trillion in revenue from $2 quadrillion in value flow, supported by 3.6 trillion transactions worldwide.

The infrastructure powering these transfers, payment rails, determines not just how fast money moves, but how much arrives at its destination.

The entire payment process has been reimagined, from initiation to settlement, creating opportunities that didn't exist five years ago. The shift from legacy systems to digital payments has fundamentally changed how businesses approach both domestic payments and international transfers.

For companies operating internationally, understanding and optimizing payment methods across different rails has become the difference between thriving and merely surviving in the digital economy.

The question isn't whether to modernize your payment infrastructure, but which rails will give you competitive advantage in an increasingly connected world.

What are payment rails and how do they work?

Payment rails are the infrastructure networks that enable money movement between financial institutions, businesses, and individuals. Think of them as highways from which money can pass through.

Each payment rail operates with distinct capabilities and constraints that determine which transactions it can handle: Some rails process unlimited transaction amounts; regulatory requirements differ, with some demanding extensive documentation; certain networks operate exclusively in domestic currency; and operating hours vary dramatically, with traditional ACH systems run on business day schedules, while modern instant payment systems process transactions 24/7/365.

Core components of payment rails

Every payment that moves through a rail follows five critical stages, and understanding each one helps you identify where delays and costs creep into your payment processing operations:

- Initiation: The payment journey begins when a business or individual creates a payment instruction, whether through a banking portal, API call, or payment platform.

- Authorization: The system verifies the payer has sufficient funds and proper permissions to execute the transaction.

- Clearing: Payment instructions are exchanged and reconciled between financial institutions, ensuring every debit matches a corresponding credit.

- Settlement: The actual transfer of funds occurs between institutions through central bank accounts or commercial arrangements.

- Confirmation: Final notification confirms successful completion to all parties, enabling reconciliation and accounting.

What makes modern rails like RTP in the US, PIX in Brazil, SPEI in Mexico, and Bre-B in Colombia, revolutionary, is how they've integrated all five stages of the process instantly through event-driven architectures and sophisticated APIs, operating 24/7/365.

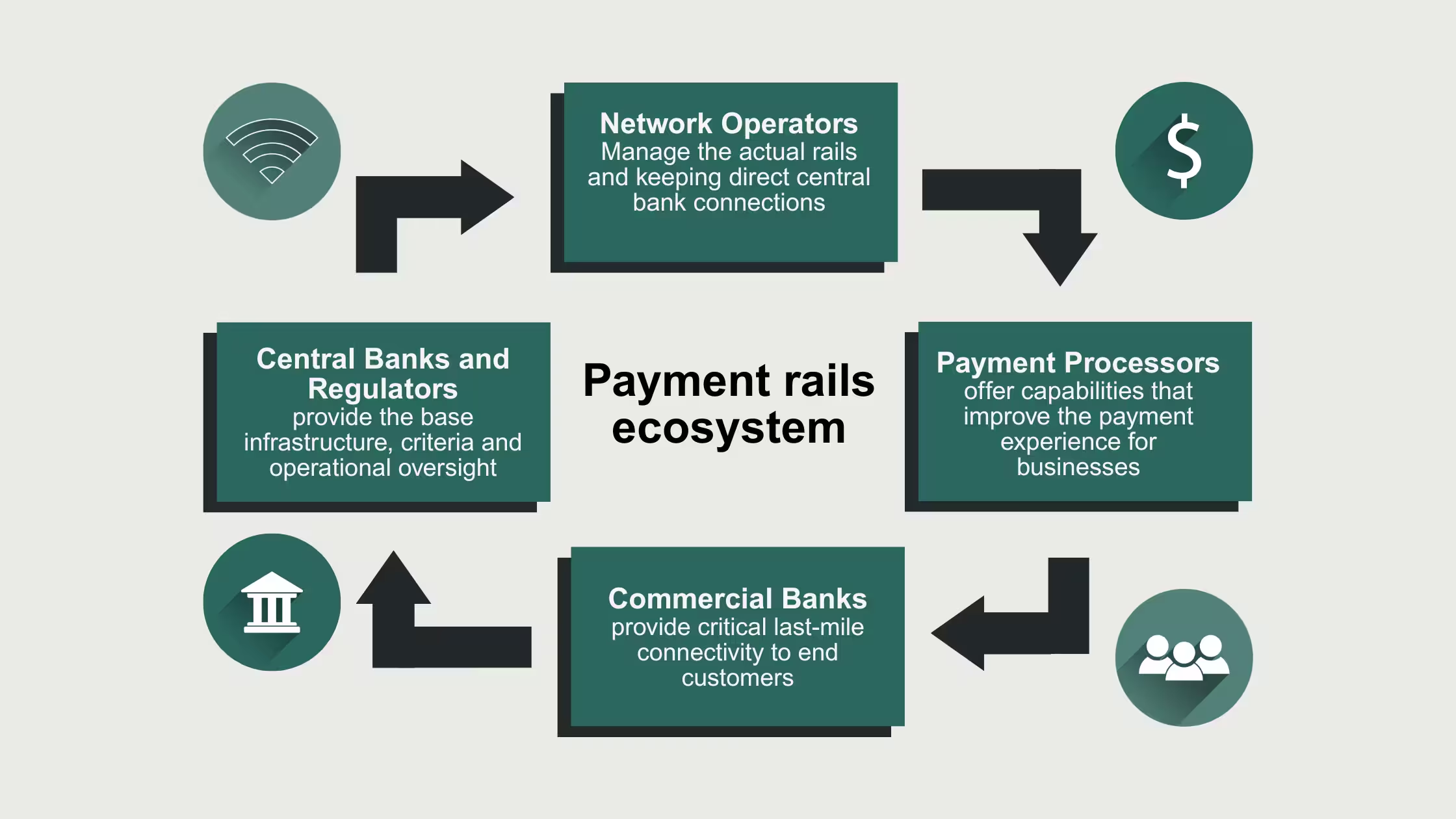

Who are the key players in the payment rails ecosystem?

The payment rails ecosystem brings together multiple participant types, each essential to global money movement.

Understanding their roles helps identify optimization opportunities and potential partnerships:

The payment rails ecosystem functions through four stages:

- Payment processors, whose main purpose is to offer capabilities for improving the payment experience for businesses.

- Commercial banks provide last-mile connectivity to end customers.

- Central banks and regulators are the ones in charge of providing infrastructure, criteria and operational oversight.

- Last but not least, network operators are the ones in charge of managing the actual payment rails and maintaining the connection to central banks.

The key insight? Today's winners don't compete on exclusive access but on interoperability.

Leading infrastructure providers excel at connecting disparate systems seamlessly, creating network effects that benefit all participants.

At Cobre, we’ve built direct connections to Latin America’s most advanced payment rails, giving companies simple access to payment services so they can focus on scaling their entire business, with a trusted partner for domestic and international payments.

What are the major global payment rail networks?

The networks powering commerce between North and Latin America fall into four primary categories: international wire transfers via SWIFT, ACH and domestic bank transfers, debit and credit card networks (Visa, Mastercard, American Express) and real-time payment systems (RTP, FedNow, PIX, SPEI).

1. International wire transfers via SWIFT

The SWIFT network (Society for Worldwide Interbank Financial Telecommunication), remains the primary infrastructure for global commerce, connecting over 11,000 institutions and processing US$150 trillion annually. While it offers unparalleled reach, its legacy architecture presents specific challenges for modern treasury management:

- Complex fee structure: Beyond the flat wire fee, the "correspondent banking" model allows intermediaries to deduct percentage-based fees and apply FX markups, often resulting in an opaque final cost.

- Settlement latency: Standard transactions require 1–4 business days. Any discrepancy in payment instructions triggers manual intervention, extending timelines and impacting working capital.

- Global standardized messaging: Its main advantage is the ability to handle any currency pair through a secure, standardized messaging protocol, making it indispensable for high-value, non-routine transfers.

- The shift to modern alternatives: While banks use SWIFT as the default backend, specialized payment platforms now offer direct integration into regional real-time rails. These alternatives provide transparent pricing and near-instant settlement without compromising institutional security.

2. ACH and domestic bank transfers

ACH (Automated Clearing House) powers North American commerce, processing US$72 trillion through 30 billion transactions annually at just US$0.20-1.50 per transaction. But efficiency comes with tradeoffs:

- Standard ACH prioritizes low-cost transactions upon fast money movement, so settlement happens within 3 working days. It also operates on batch schedules, meaning payments submitted Thursday afternoon might not clear until Tuesday.

- Same Day ACH transfers offer settlement within hours for an additional fee, typically representing a small percentage premium over standard ACH. This option processed 854 million transactions worth US$2.5 trillion in 2024.

3. Debit and credit card networks

Card rails like Visa, Mastercard and American Express, offer instant authorization and global acceptance at 100+ million merchants, solving the "last mile" problem other rails struggle with and it's extremely useful when suppliers don't accept other payment methods or when immediate authorization is critical.

This ubiquity creates a superior payment experience for consumers, but for B2B transactions, card fees of 2.5-3.5% per transaction become prohibitively expensive at scale.

4. Real-time payment systems (RTP, FedNow)

A payment system is a specialized set of instruments, banking procedures, and interbank funds transfer networks that ensure the circulation of money within an economy.

The United States infrastructure has evolved toward instant finality through two primary networks: RTP (The Clearing House) and FedNow (Federal Reserve).

- RTP: Reaching approximately 90% of US demand deposit accounts, RTP settles transactions in under 2 seconds. With a transaction limit of $10 million USD and costs ranging from $0.25 to $1.00, it has become a primary rail for large-scale B2B liquidity management.

- FedNow Service: Launched by the Federal Reserve to connect over 9,000 institutions, it offers a lower transaction limit of $500,000 USD but higher cost-efficiency, with fees between $0.01 and $0.50.

Although over 10,000 institutions have access via the Federal Reserve, only a fraction actively process instant payments. This creates a strategic need for infrastructure providers that can guarantee "always-on" capabilities regardless of a specific bank's internal limitations.

Unlike the fragmented adoption in the US, Latin American systems like PIX in Brazil, SPEI in Mexico, and Bre-B in Colombia are central bank-mandated infrastructures.

These rails benefit from being central-bank sponsored infrastructures, allowing for billion-transaction scale settlements in less than a minute.

For companies operating across the Americas, leveraging advanced regional rails through a single API provider eliminates the friction of domestic banking silos and optimizes working capital through immediate settlement finality.

5. The new financial infrastructure: stablecoins as a payment method

Stablecoins are digital assets pegged to a fiat currency (such as the dollar) that operate on blockchain technology. With stablecoin regulations like the GENIUS Act (2025) and Europe’s MiCA regulation, these digital assets have transitioned from speculative instruments into regulated, legitimate payment rails for corporate treasuries.

The GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins) marked a turning point by establishing three core pillars:

- Liquid Backing: Mandatory 1:1 reserves held in cash or U.S. Treasury bonds.

- Transparent Audits: Monthly reports verified by independent third parties.

- National Security: Integration of AML (Anti-Money Laundering) protocols directly into the asset's code.

This framework allows companies to use stablecoins like USDC for immediate B2B payments, settling global transactions at near-zero costs while eliminating the volatility risk that plagued first-generation cryptocurrencies.

You can read more about what are stablecoins, and their regulatory requirements.

Technical components of a modern payment rail

For a company to be resilient, its infrastructure must be based on six pillars that guarantee interoperability:

- Central banks: They act as the ultimate trusted node and operators of RTGS systems.

- Technical layer processors: Entities that translate business needs into executable code (API instructions).

- Clearing houses: They act as the central "switchboard" that ensures that balances between banks are perfectly synchronized.

- API (Application Programming Interfaces): The connection layer that allows companies' ERP systems to "talk" directly to payment rails, eliminating manual burden.

- Security protocols: Use of HSM (Hardware Security Modules) and TLS 1.3 encryption to protect the movement of sensitive data.

Data formats (ISO 20022): The universal language that allows a payment to carry detailed billing information, facilitating automatic reconciliation.

Who supports validation across ACH, RTP, PIX and SPEI rails?

Validation is the critical layer that prevents failed transactions and operational friction. In a multi-rail environment with regional vendors, support can come in payment infrastructures Modern infrastructure layers like Cobre act as a unified validation gate.

Instead of businesses manually managing fragmented protocols—such as Colombia’s Bre-B, Mexico’s SPEI, or global ACH networks—Cobre’s API performs automated pre-transaction checks. This process ensures accuracy by verifying:

- Bank Codes & Account Structures: Confirming the destination is reachable.

- Local Identity Requirements: Validating specific tax IDs like RFC (Mexico) or NIT (Colombia).

By centralizing validation, businesses eliminate the manual overhead of "repairing" rejected payments and mitigate the risks associated with manual data entry in cross-border operations.

When adopting payment rails, it is important for a business to take into consideration aspects such as scalable operation and compliance. This is where ISO 20022 comes into play.

By utilizing structured data, organizations can minimize manual intervention and strengthen compliance, ultimately reducing operational overhead.

How is the ISO 20022 standard changing the rules of the game?

The ISO 20022 standard is a universal and enriched language for the exchange of financial data, facilitating automation, reconciliation, and improved regulatory compliance.

Unlike older formats such as SWIFT MT, ISO 20022 allows structured and extensive metadata to be included in each payment message.

With the global transition to ISO 20022, payment rails now carry:

- Legal Entity Identifiers (LEI): For complete transparency about who is sending and who is receiving.

- Structured remittance data: Detailed breakdown of multiple invoices, credit notes, and discounts in a single payment message.

- Payment purpose: Standardized codes that facilitate risk monitoring and reporting to regulators without human intervention.

This is where infrastructure providers demonstrate their value beyond simple connectivity.

Through infrastructure providers, like Cobre's Local Payments solution, companies can operate continuously, with a platform automatically capturing required regulatory data, performing validations, and maintaining audit trails across all payment types.

To summarize …

The payment landscape has reached an inflection point. While SWIFT still processes $150 trillion USD annually, stablecoins handle $27 USD trillion, and Latin American instant payment systems demonstrate what's possible when infrastructure is designed for modern multi rail commerce rather than retrofitted from legacy systems.

The opportunity is immediate and measurable. Companies leveraging multi-rail strategies report dramatic reductions in cross-border costs, 70% faster reconciliation, and working capital improvements exceeding 20%.

The path forward requires three critical decisions.

- First, acknowledge that payment infrastructure is now a competitive differentiator, not just operational plumbing.

- Second, recognize that Latin America often leads in payment innovation, offering capabilities that surpass what's available domestically.

- Third, partner with providers who abstract complexity while delivering flexible payments orchestration strategies.

At Cobre, we've built direct connections to advanced payment rails in Mexico and Colombia, SPEI and Bre-B, systems that demonstrate the power of instant payment infrastructure designed for modern commerce, similar to how Brazil's PIX has transformed that market. All of this is accessible through a single API.

This means your expansion into Latin America doesn't require months of bank negotiations, complex integrations, or navigating regulatory mazes across multiple countries.

Instead, you gain immediate access to infrastructure already processing $10 billion USD annually, instant payment capabilities that outperform US systems, and local expertise that turns payment complexity into competitive advantage.

Whether you're paying suppliers in Mexico, collecting from customers in Colombia, or managing treasury across the entire region, you leverage the same infrastructure that enables 300+ companies to operate seamlessly across borders.

The rails are ready. The technology is proven. The only variable is how quickly you'll move to capture the advantage.

FAQs about payment rails

What is a payment rail?

A payment rail is the infrastructure network that enables money movement between banks, businesses, and individuals. Like highways for money, payment rails include systems such as ACH, wire transfers, card networks, and instant payment systems that process, clear, and settle financial transactions.

Are there payment rails for developing countries?

Companies in Latin America operate in a multi-rail approach.

Through a single API or Portal, businesses access multiple rails across the region for local and international transfers like: traditional ACH networks, and instant payment systems like PIX in Brazil, SPEI in Mexico, and Bre-B in Colombia,

These local payment systems offer capabilities that often complement what’s available in North American markets and provide additional infrastructure for businesses operating in the US and Latin America.

Is PayPal a payment rail?

No, PayPal is not a payment rail but a payment service provider that uses existing rails like ACH, card networks, and wire transfers to move money. PayPal aggregates multiple payment rails behind its platform, making it easier for users to send and receive payments without directly accessing the underlying infrastructure.

Nonetheless, PayPal can be expensive, particularly for international transfers, credit card funding or currency conversions, where fees can range from 3% to 5%.

Is Mastercard a payment rail?

Yes, Mastercard operates one of the world's largest payment rails, processing over 100 billion transactions annually. The Mastercard network connects issuing banks, acquiring banks, and merchants globally, enabling instant authorization and settlement of card-based payments through its proprietary infrastructure.

Is SWIFT a payment rail?

Yes, SWIFT is a major international payment rail processing $150 trillion annually across 11,000+ financial institutions in 200 countries. It provides the messaging infrastructure and standards that enable banks to execute cross-border money transfers and international payments between different currencies.

Is ACH a payment rail?

Yes, ACH (Automated Clearing House) is a foundational payment rail in the United States, processing $77 trillion through 30 billion transactions annually. This electronic network enables direct bank-to-bank transfers for payroll, bill payments, and B2B transactions at low costs of $0.20-1.50 per transaction.

Is Colombian ACH different from USA ACH?

Yes. While both are payment rails, they represent different types of entities:

- In the United States: ACH is the name of the standardized national network itself, governed by Nacha and the Federal Reserve. It is the infrastructure used by all banks to process batch payments.

- In Colombia: ACH refers to ACH Colombia, a private company founded by local banks to provide the technological "pipes" that allow money to move between institutions.

Key difference in speed: Unlike modern instant rails, traditional ACH in both countries relies on batch processing. In Colombia, moving money through this specific rail is not immediate; depending on the time the transaction is initiated, it can take up to 3 business days to settle.

In Cobre, we offer a more efficient solution: Fast Pay, which is a modernized payment rail designed for continuous, real-time processing. Unlike traditional systems that rely on scheduled time slots, Fast Pay allows businesses to execute payment disbursements with greater speed and predictability.